Silver occupies a unique position in global markets acting as both a precious metal and an essential industrial material, giving it exposure to two powerful demand drivers simultaneously. Its role in wealth preservation has endured for thousands of years, while its industrial relevance continues to grow as the global economy electrifies and decarbonises.

This combination makes silver distinct from many other commodities. It can benefit from demand linked to renewable energy, electronics, and advanced manufacturing, while also attracting interest as a store of value and portfolio diversifier during periods of inflation, uncertainty, and geopolitical risk.

Silver’s appeal is therefore not limited to its industrial role. It is also viewed as a hedge against inflation, a liquid globally recognised asset, and a store of value with a long monetary history. That broader investment relevance matters because it means silver can attract demand from more than one source. It may benefit when industrial activity expands, but it can also draw interest during periods of market uncertainty when investors seek tangible assets and exposure to precious metals.

Silver’s physical properties make it exceptionally valuable across a wide range of modern applications. It has the highest electrical and thermal conductivity of all elements, is highly reflective, and is widely used in technologies where efficient energy transfer and material performance are critical.

Industrial demand already accounts for a large share of total silver consumption, and that demand has strengthened as investment in decarbonisation and electrification continues to accelerate. As more economies expand renewable power generation, upgrade electrical systems, and deploy advanced technologies, silver’s industrial role is expected to remain central.

Solar/Photovoltaics

Electronics & Electrilcal

Electric Vehicles & Charging Infrastructure

Artificial Intelligence

Data Centres

Advance Computing

Medical & Antimicrobial Applications

Water Purification

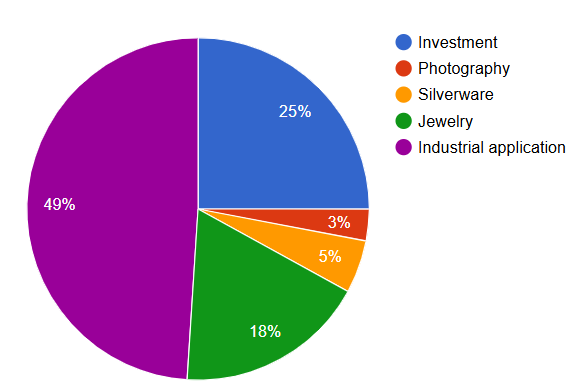

Jewelry

Silver continues to attract investor interest as a liquid, globally recognised hard asset. In periods of inflation, financial volatility, and geopolitical uncertainty, it is often viewed as a practical way to preserve value and diversify portfolio exposure.

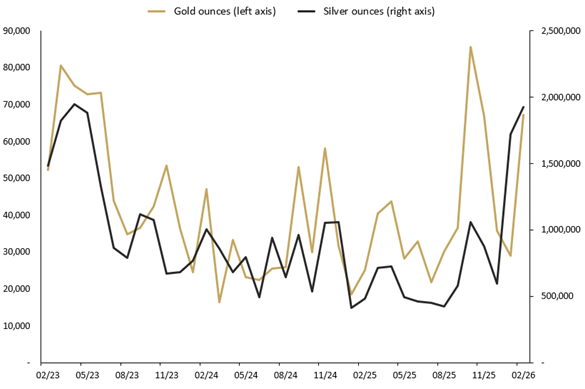

Its accessibility also adds to that appeal. Relative to gold, silver offers more affordable entry to the precious metals market while still benefiting from strong liquidity and global recognition. That demand has been particularly evident in recent Perth Mint data. In February 2026, the Mint sold 1.92 million ounces of silver in minted product form, with silver sales up 120% over three months and 299% over twelve months, while also reporting strong retail demand across all key regions.

This matters because strong investor demand adds another layer of support to silver at a time when industrial demand is also rising. When both sides of the market strengthen together, silver’s long-term investment case becomes even more compelling.

One of the clearest drivers of silver demand is its use in solar photovoltaic technology. Solar demand for silver has reached around 200 million ounces annually, accounting for a significant share of total global silver consumption and reflecting the scale of global solar deployment, including rapid growth in China and the broader push toward cleaner electricity systems.

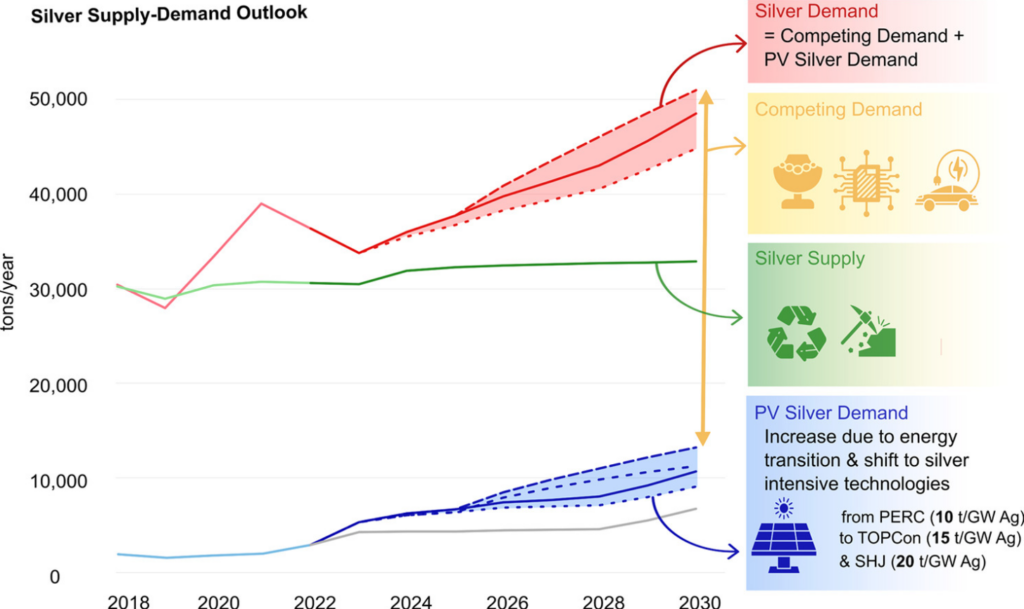

Recent research reinforces how important this relationship may become over the rest of the decade. A 2026 study in Resources, Conservation and Recycling found that the solar industry is expected to be the fastest-growing source of silver demand through 2030, with annual photovoltaic demand projected to reach 10,000-14,000 tonnes per year, equivalent to roughly 29-41% of projected silver supply. The study also found that total silver demand could materially outpace available supply by 2030, with supply meeting only 62-70% of projected demand under its scenarios.

This matters because solar demand is being driven not only by more installations, but also by the changing technology mix within solar manufacturing. Crystalline silicon technologies dominate the market, and newer high-efficiency cell types such as TOPCon and SHJ are more silver-intensive than older PERC cells. According to the study, TOPCon cells use about 1.5 times as much silver per gigawatt as PERC, while SHJ cells use about 2 times as much.

As the energy transition continues, the relationship between silver and solar is likely to remain one of the most important long-term demand drivers for the metal. Silver is not simply benefiting from cyclical industrial activity; it is tied to structural trends reshaping the global energy system, and emerging research suggests those trends could intensify competition for available supply over the coming decade.

Source: Cattaneo, V. et al. (2026). Forecasting silver demand and supply by 2030: Impact of silver-intensive photovoltaic cells and sectoral competition. Resources, Conservation and Recycling, 224, 108562.

Silver plays an important role in electric vehicles and the broader electrification of transport. Its unmatched electrical conductivity makes it valuable in vehicle electronics, power management systems, charging infrastructure, and the growing network of technologies needed to support a more electrified economy. As transport systems become more advanced and more dependent on efficient electrical performance, silver’s relevance continues to increase.

This matters because the transition to electric vehicles is not an isolated trend. It sits within a much larger shift toward electrification, grid expansion, and more sophisticated energy systems, all of which require materials that can reliably transmit power and support high-performance components. For silver, that creates another structural source of long-term industrial demand alongside solar and electronics.

Silver is also increasingly relevant to the rise of artificial intelligence, advanced computing, and data-intensive digital infrastructure. AI systems rely on powerful processors, high-performance electronics, and expanding data centre capacity, all of which increase the need for efficient electrical materials in advanced electronic systems. Silver’s conductivity and performance characteristics make it well suited to these high-tech applications.

As investment in AI infrastructure accelerates, silver stands to benefit from another long-term technology trend beyond traditional industrial demand. This strengthens its position as a metal linked not only to the energy transition, but also to the continued expansion of next-generation computing, connectivity, and digital infrastructure.

Silver’s long-term outlook is also shaped by tightening market fundamentals. Annual silver consumption is approximately 1,240 million ounces, compared with annual mine production of 820 million ounces, with 82% of annual supply sourced from mining and 18% from recycling.

Metals Focus supply-and-demand data also shows sustained deficits in recent years, with the market balance remaining negative across multiple consecutive years. This reinforces the broader view that silver demand has been exceeding new supply, particularly as industrial use has expanded.

That supply picture is made more fragile by the structure of the silver market itself. Because much of the world’s silver is produced as a by-product of mining for other metals, supply cannot simply be increased in response to higher demand. In many cases, silver is not the primary commodity being targeted, which limits the industry’s ability to respond quickly when shortages emerge.

As demand continues to rise faster than mine supply, pressure builds on available above-ground stocks. In that environment, silver’s scarcity becomes increasingly important to long-term price support.

| YEAR | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Million ounces | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025F | 2024 | 2025F |

Supply | ||||||||||||

| Mine Production | 900.1 | 863.9 | 850.8 | 837.4 | 783.8 | 830.8 | 839.4 | 812.7 | 819.7 | 835.0 | -1% | 2% |

| Recycling | 156.3 | 160.2 | 162.3 | 163.8 | 180.5 | 190.7 | 193.5 | 183.5 | 193.9 | 193.2 | 6% | 0% |

| Net Hedging Supply | 0.0 | 0.0 | 0.0 | 13.9 | 8.5 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | na | na |

| Net Official Sector Sales | 1.1 | 1.0 | 1.2 | 1.0 | 1.2 | 1.5 | 1.7 | 1.6 | 1.5 | 1.5 | -9% | -4% |

| Total Supply | 1,057.4 | 1,025.1 | 1,014.2 | 1,016.2 | 974.0 | 1,023.1 | 1,034.6 | 997.8 | 1,015.1 | 1,030.6 | 2% | 2% |

| Demand | ||||||||||||

| Industrial (total) | 491.0 | 528.0 | 525.8 | 523.4 | 511.9 | 564.1 | 592.3 | 657.1 | 680.5 | 677.4 | 4% | 0% |

| Electrical & Electronics | 309.0 | 339.1 | 330.4 | 326.6 | 321.4 | 350.7 | 370.7 | 444.4 | 460.5 | 465.6 | 4% | 1% |

| … of which photovoltaics | 81.6 | 99.3 | 87.0 | 74.9 | 82.8 | 88.9 | 118.1 | 192.7 | 197.6 | 195.7 | 3% | -1% |

| Brazing Alloys & Soldiers | 49.1 | 50.9 | 52.0 | 52.4 | 47.5 | 50.5 | 49.2 | 50.2 | 51.6 | 52.9 | 3% | 3% |

| Other Industrial | 132.9 | 138.0 | 143.5 | 146.4 | 142.9 | 162.9 | 172.4 | 162.6 | 168.4 | 158.9 | 3% | -6% |

| Photography | 34.7 | 32.4 | 31.4 | 30.7 | 26.9 | 27.7 | 27.7 | 27.3 | 25.5 | 24.2 | -7% | -5% |

| Jewelry | 189.1 | 196.2 | 203.2 | 201.6 | 150.9 | 182.0 | 234.5 | 203.1 | 208.7 | 196.2 | 3% | -6% |

| Silverware | 53.5 | 59.4 | 67.1 | 61.3 | 31.2 | 40.7 | 73.5 | 55.1 | 54.2 | 46.0 | -2% | -15% |

| Net Physical Investment | 212.9 | 155.8 | 165.9 | 187.4 | 208.1 | 284.3 | 338.3 | 244.3 | 190.9 | 204.4 | -22% | 7% |

| Net Hedging Demand | 12.0 | 1.1 | 7.4 | 0.0 | 0.0 | 3.5 | 17.9 | 11.5 | 4.3 | 0.0 | -62% | na |

| Total Demand | 993.3 | 972.9 | 1,000.8 | 1,006.4 | 929.0 | 1,102.4 | 1,284.2 | 1,198.5 | 1,164.1 | 1,148.3 | -3% | -1% |

| Market Balance | 64.1 | 52.2 | 13.5 | 9.8 | 45.1 | -79.3 | -249.6 | -200.6 | -148.9 | -117.6 | -26% | -21% |

| Net Investment in ETPs | 53.9 | 7.2 | -21.4 | 83.3 | 331.1 | 64.9 | -117.4 | -37.6 | 61.6 | 70.0 | na | 14% |

| Market Balance less ETPs | 10.2 | 45.1 | 39.9 | -73.5 | -286.1 | -144.3 | -132.2 | -163.0 | -210.5 | -187.6 | 29% | -11% |

| Silver Price (US$/oz, London price) | 17.14 | 17.05 | 15.71 | 16.21 | 20.55 | 25.14 | 21.73 | 23.35 | 28.27 | - | 21% | na |

| Source: Metals Focus | ||||||||||||

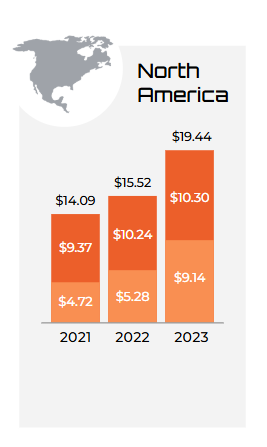

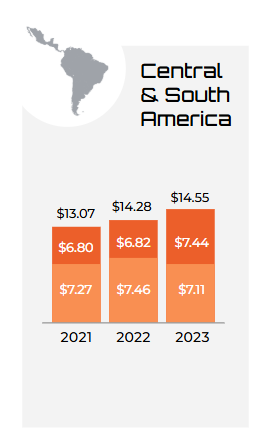

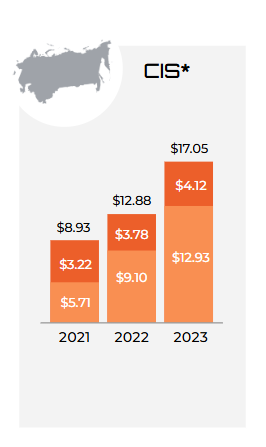

Another important part of the silver market story is the rising cost and increasing difficulty of bringing new supply to market. All-in sustaining costs continue to climb across major mining regions, reaching $19.44/oz in North America, $17.05/oz in CIS countries, $14.55/oz in Central and South America, and $8.91/oz in Asia in 2023.

Over the past half century, volatility and uncertainty in the long-term silver price have also made it difficult for many silver mines to establish themselves and sustain profitability. This has reduced confidence in long-term mine development, contributed to a more fragile supply base, and helped drive the significant supply deficit currently affecting the silver market. The issue is further intensified by the long lead times required to bring new silver projects into production, meaning supply cannot be increased quickly even when demand rises.

This is positive for silver because it strengthens the long-term supply-demand outlook for the metal. Where new supply is both expensive and difficult to bring online, sustained demand growth has a greater impact on market balance, helping reinforce silver’s scarcity and providing stronger long-term support for price appreciation.

Silver sits at the intersection of some of the most powerful forces shaping the global economy: the transition to clean energy, the expansion of electrification, rising industrial demand, and growing investor interest in scarce tangible assets. At the same time, supply remains under pressure from persistent deficits, limited primary silver production, rising costs, and the long timelines required to bring new projects online.

These conditions make silver increasingly important and give it compelling long-term upside. With demand strengthening across both industrial and investment markets while supply remains difficult to expand, silver is well positioned to benefit from tightening market fundamentals and growing strategic relevance in the years ahead.